The effect of time series stability in estimating the investment function

Keywords:

Time series stability, ,investment functionAbstract

Stabilizing effectofthetimeseriesto estimate thefunctionofinvestmentinIraq It is known, for example, that the t-statistic tables are designed primarily to deal with the results of the regression that uses static chains. This has been the former treats .assumption until the mid-seventies, where researchers are conducting studies applied without taking into account the characteristics of the time series used by an appreciation, was to accept the results of these tests and Bmanueh delivery capabilities based on the application of the theory of statistical inference on these estimators.

But the scientists Granger and Newbold 1974 generate random time series is static Stationary Non (specifically conduct random strings) using simulation method these chains do not express any unknown variable and then considered these independent chains. They then conducted a large number of regression estimates using these

strings on each other. After appreciation was calculated values statistical t Under the assumption that the parameter true zero (ie the parameter estimates of regression likes to be insignificant to the independence and random variables used in the estimate), but despite the real that the time series were random and independent, the researchers found that the zero hypothesis that the real parameter is equal to zero was rejected by repeating or greater likelihood than what theory predicts significant relationship was accepted from a statistical point of view, researchers also noted that the residuals resulting from regression estimates by a large self positive correlation.

The researchers thus reach to an important result and that serious estimators and statistical tests that result from time-series regressions used is still considered the results of improper or false decline spurious regressions can not be reassuring to the results of statistical inference on its resources. The form of this research a starting point for new research in the field of sleep test series, cast doubt on the results of all previous standard tests used the time series properties did not take into account the

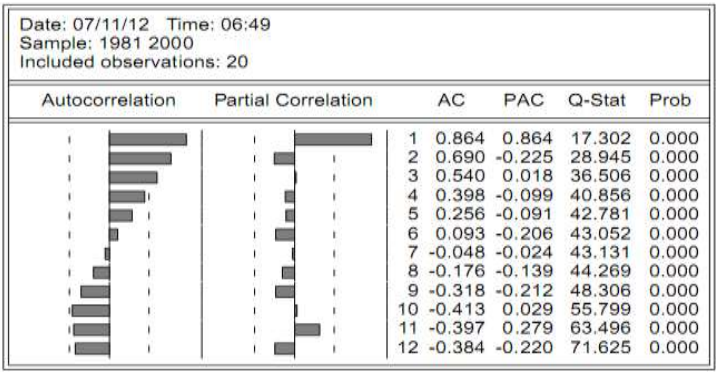

time-series before appreciation. Then came all of Engel and Granger 1987 to decide that in the case of single or sole exception are results of the assessment is fake and can apply the rules of statistical inference in the case estimate slope using two strings is, which is that leftover estimate regression equation be static, and say then that the two strings of two integration Even Co-Integration.). And on this basis was used standard methods to test stability of the time series of the variables used to estimate the function of investment in Iraq and then test their conformity to the integration of the joint in order to reach the best model for this function, which reflects the reality of investment in Iraq for the period (1982-2000)

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2013 Economics and Administration College - Karbala University

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

Authors retain the copyright of their papers without restrictions.