Simple methods to build optimal equity portfolios

Abstract

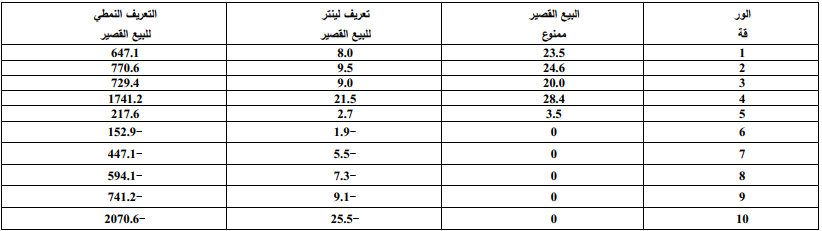

Several models (factor models and group models) were developed to simplify the inputs to the Markowitz's portfolio selection problem. Each of these models makes an assumption about why stocks co-vary together. Each lead to a simplified structure for the correlation matrix or covariance matrix between securities. These models were developed to cut down on the number of inputs and simplify the nature of the inputs needed to forecast correlations between securities. The use f these models was expected to lead to some loss of accuracy in forecasting correlations, but the ease of using the models was expected to compensate for this loss of accuracy. However, empirically confirm that when fitted to historical data, these simplifying models result in an increase, not a decrease, in forecasting accuracy. The models are of major interest because they both reduce and simplify the inputs needed to perform portfolio analysis and increase the accuracy with which correlations and covariances can be forecast. This paper is discussed several simple rules for optimal portfolio selection. Its reached to many of conclusions, most important among them is these simple techniques (which are based on the single index model and constant correlation model) allow the portfolio manager to quickly and easily determine the optimum portfolio. Furthermore, the manager uncertain about some of the estimates can easily manipulate them in order to determine if reasonable changes in the estimates lead to a different selection decision. This paper is reached to many recommendations, most important among them is that financial assets should be evaluated on the basis of their expected returns and risk and that portfolio expected return and risk can be calculated based on these inputs and the covariances involved. Calculation of portfolio risk is the key issue. Since the complete Markowitz covariance analysis is very complicated and needed to huge calculations, investors and portfolio managers working in the Iraqi stock exchange should be use the single factor model or constant correlation model to simplify and reduce quantity and quality of inputs needed to the analysis, especially these simplifying models are merit confirmed on the both theoretical and practical levels.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2012 Iraqi Journal for Administrative Sciences

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

Authors retain the copyright of their papers without restrictions.