Applying Artificial Intelligence Techniques in Accounting to Improve the Quality of Financial Reports

A Survey of The Opinions of a Sample of Academics, And Professionals in Iraq

DOI:

https://doi.org/10.71207/ijas.v22i87.5306Keywords:

Financial Report Quality, Artificial IntelligenceAbstract

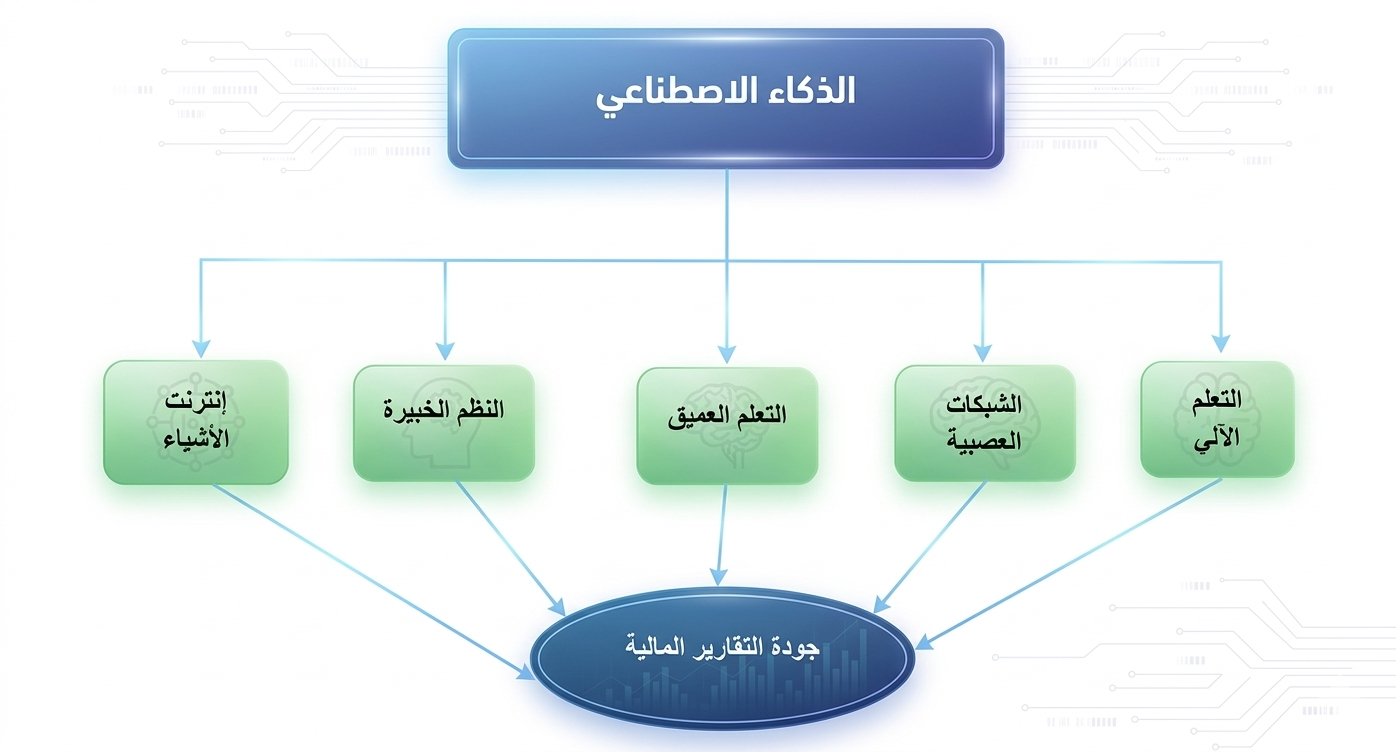

The primary objective of applying artificial intelligence (AI) technologies, as an information technology component, is to enhance the quality of financial reporting. This is achieved through AI's advanced capabilities in classifying, processing, and analyzing financial data with high accuracy and speed. These technologies contribute to the early detection of potential risks, as well as their role in continuously verifying the integrity of financial data and implementing precise and effective control systems for financial operations. This, in turn, helps reduce the likelihood of manipulation, forgery, and financial fraud. Furthermore, AI technologies possess advanced predictive capabilities that support decision-making processes. This, in turn, enhances the confidence of decision-makers by providing high-quality financial reports supported by AI-based analytics, thereby increasing transparency in handling financial data. The research comprised two main aspects: a theoretical framework and an applied framework. The research employed a descriptive-analytical approach to analyze variables and test hypotheses. To collect data, a questionnaire was used, distributed to a sample of accountants and auditors as the primary group, in addition to a sample of programmers. The number of valid responses for analysis was 121. The SmartPLS statistical software was used to analyze the data and test the research model. The research results indicated a significant positive impact of artificial intelligence technologies (machine learning, deep learning, neural networks, expert systems, and the Internet of Things) on improving the quality of financial reports.

Downloads

References

1. بهانة، وداد محمد حساني (2023). دور الإفصاح المحاسبي الإلكتروني كمتغير وسيط في العلاقة بين تقنيات الذكاء الاصطناعي وجودة التقارير المالية: دراسة ميدانية على الوحدات الاقتصادية المقيدة في البورصة المصرية. مجلة المحاسبة والمراجعة لاتحاد الجامعات العربية، 10(1):377-426.

2. علي، عبد الوهاب نصر (2022). مهنة المحاسبة في مواجهة تداعيات التحول الرقمي في مصر (قصور الممارسة وحتمية التطوير). المجلة العلمية للدراسات والبحوث المالية والإدارية .13(2) , 15-25.

3. القشاوي، مريم الرفاعي محمد عبد الرحمن (2022). دراسة تحليلية لتقييم دور تقنيات الذكاء الاصطناعي في تحسين عملية الافصاح المحاسبي الالكتروني. مجلة البحوث الادارية والمالية والكمية ،2(2) :82-96.

4. لحمر هيبة (2021). التحول الى الذكاء الاصطناعي بين المخاوف والتطلعات التجربة الامارتية نموذجا، مجلة الاقتصاد والتنمية، المجلد 09، العدد 02، ص ص 97-99.

5. Shirazi, M. (2020). Will artificial intelligence end the job of financial auditor in the midst of the revolution. BMA Journal.

6. Hasan, A. R. (2021). Artificial intelligence (AI) in accounting and auditing: A literature review. Open Journal of Business and Management, 10(1):440- 465.

7. Rout, J.K., Choo, KK.R., Dash, A.K. et al. (2018) A model for sentiment and emotion analysis of unstructured social media text. Electron Commer Res 18, 181–199.

8. He, X. Chu, L. R. Qiu, C., Ai, Q., and Z. Ling, 2018. A novel data-driven situation awareness approach for future grids-using large random matrices for big data modeling, IEEE Access, vol. 6, pp. 13855-13865.

9. Xiaofang, Z. (2021). Application of data mining and machine learning in management accounting information system. Journal of Applied Science and Engineering, 24(5), 813-820.

10. Ben-Daya, M., Hassini, E., & Bahroun, Z. (2019). Internet of things and supply chain management: a literature review. International Journal of Production Research, 57(15-16), 4719-4742.

11. Hsu, Y. L., & Yang, Y. C. (2022). Corporate governance and financial reporting quality during the COVID-19 pandemic. Finance Research Letters, 47, 102778.

12. Khalil, U. F. (2022). Auditor choice and its impact on financial reporting quality: A case of banking industry of Pakistan. Asia Pacific Management Review, 27(4), 292-302.

13. Paydar, S. R., & Babalou, F. (2019). Investigating Financial Reporting Transparency. Singaporean Journal of Business Economics and Management Studies, 6(12), 18-27.

14. Harrison, W. T., Horngren, C., Thomas, B., Suwardy, T. (2013). Financial Accounting: Global Edition. United Kingdom: Pearson Education Limited.

15. Pfeiffer, G. M., Dyckman, T. R., Hanlon, M. L., Morse, W. J., Magee, R. P., Hartgraves, A. L. (2020). Financial & Managerial Accounting for MBAs. United States: Cambridge Business Publishers.

16. Kieso, D. E., Weygandt, J. J., Warfield, T. D. (2019). Intermediate Accounting. United Kingdom: Wiley.

17. Hair, J., Hollingsworth, C. L., Randolph, A. B., & Chong, A. Y. L. (2017). An updated and expanded assessment of PLS-SEM in information systems research. Industrial management & data systems, 117(3), 442-458.

18. Christ, M. H., Emett, S. A., Summers, S. L., & Wood, D. A. (2021). Prepare for takeoff: Improving asset measurement and audit quality with drone-enabled inventory audit procedures. Review of accounting studies, 26(4), 1-21.

19. Ding, K., Lev, B., Peng, X., Sun, T., & Vasarhelyi, M. A. (2020). Machine learning improves accounting estimates: Evidence from insurance payments. Review of accounting studies, 25, 1098-1134.

20. Fedyk, A., Fedyk, T., Hodson, J., & Khimich, N. V. (2021). Is Artificial Intelligence Making Audit Firms More Efficient? Journal of SSRN, (1), 1-30.

21. Li, Z., & Li Zh. (2018). The Impact of Artificial Intelligence on Accounting, advances in Social Science, Education and Humanities Research (ASSEHR), vol. 181, pp.813-816.

22. PwC. (2017). Sizing the prize: what’s the real value of AI for your business and how to capitalise?

23. Quattrone, P. (2016). Management accounting goes digital: Will the move make it wiser? Management Accounting Research, 31.

24. Türegün, N. (2019). Impact of technology in financial reporting: The case of Amazon Go. Journal of Corporate Accounting & Finance, 30(3), 90-95.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2026 مرتضى حسن خليف

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

Authors retain the copyright of their papers without restrictions.