Beyond Mean-Variance: Asymmetric Returns and Downside Risk in an Extreme Frontier Market

DOI:

https://doi.org/10.71207/ijas.v22i87.5605Keywords:

Asymmetric Returns, Extreme Frontier MarketAbstract

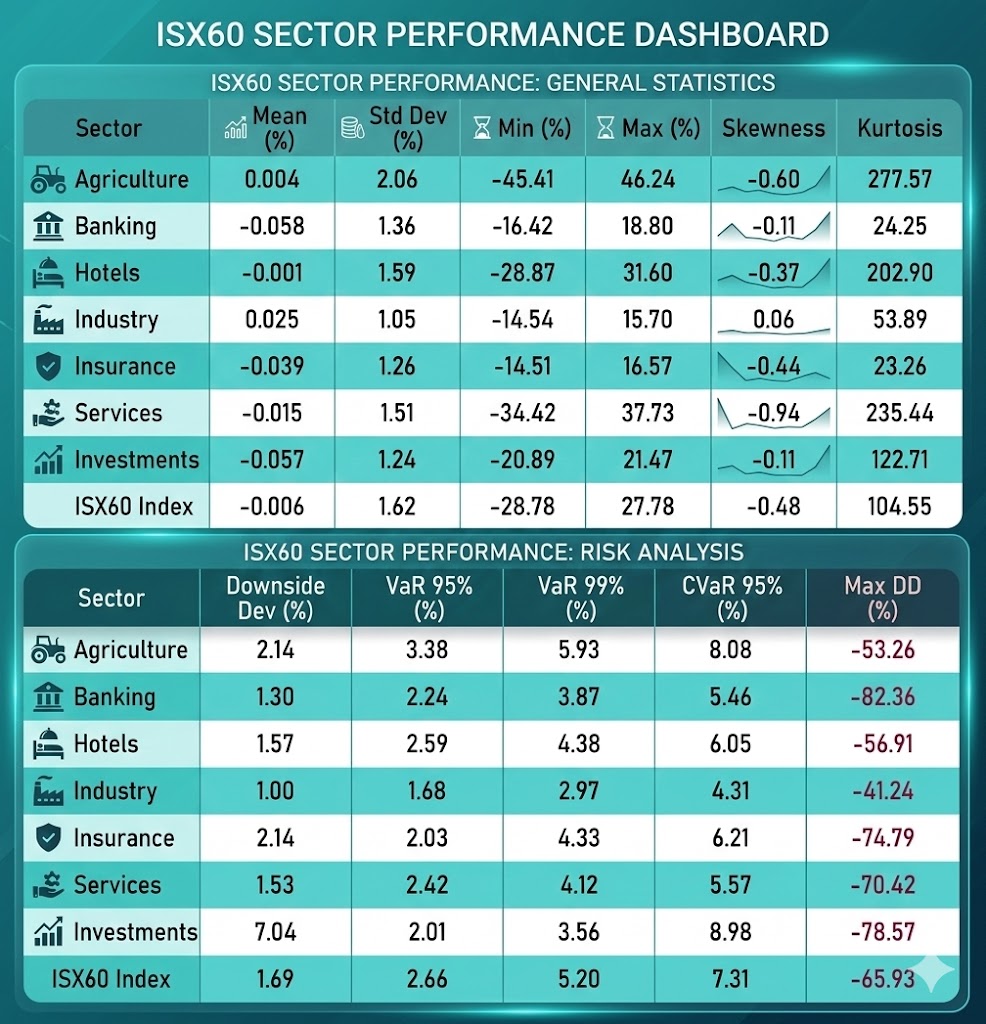

The paper is attempt to understand the asymmetry of the stock return pattern and downside risks on the Iraqi stock exchange, one of the most extreme frontier markets around the world; for the purpose of this study, we have collected and analyzed extensive daily datasets for 57 stocks on the ISX60 index, spanning August 2014 to August 2024, and through the lens of distributional analysis and the lens of various downside risk metrics (i.e., semi-variance, value-at-risk, conditional value-at-risk), and maximum drawdown, such that risk is characterized and analyzed without the usage of standard deviation). What we have discovered is that there is considerable deviation from the normal distribution across the data, where 40.4% of the stocks had a negative skewness, and an overall significant excess kurtosis (mean of 175.13) was present, such that there was no acceptance of normal distribution in our data at any conventional levels of significance. There is a noticeable discrepancy in and of itself by the varying levels of realized downside risk associated with each stock and overall across the collection of the banking sector stocks, i.e., banking sector stocks had a downside risk of an annual return of -14.55% and a maximum drawdown of -82.36% compared to the industrial stocks that have a downside risk of an annual return of +6.41% and a maximum drawdown of -41.24%. There is significant asymmetry evidenced by temporal analysis, as there is a noticeable decline in negative skewness from 61.4% of the stocks during the crisis period (2014-2018) to 26.3% during the stabilization period (2019-2024). In this high volatility environment, the Sortino ratio is a more appropriate measure of risk-adjusted performance than the Sharpe ratio. The results emphasize mean-variance optimization's shortcomings when applied to frontier markets and further reinforce the significance of incorporating measures of downside risk into the construction of portfolios and the management of risk in emerging markets with structural instability and low liquidity.

Downloads

References

1. Amaya, D., Christoffersen, P., Jacobs, K., & Vasquez, A. (2015). Does realized skewness predict the cross-section of equity returns? Journal of Financial Economics, 118(1), 135-167. https://doi.org/10.1016/j.jfineco.2015.02.009

2. Chen, X., Li, B., & Worthington, A. C. (2021). Higher moments and US industry returns: Realized skewness and kurtosis. Review of Accounting and Finance, 20(1), 1-22. https://doi.org/10.1108/RAF-06-2020-0171

3. Eissa, M. A., & Al Refai, H. (2024). Context-dependent responses to geopolitical risk in Middle Eastern and African stock markets: An asymmetric volatility spillover study. International Review of Economics & Finance, 94, Article 103402. https://doi.org/10.1016/j.iref.2024.103402

4. Ekholm, A., & Pasternack, D. (2005). The negative news threshold—An explanation for negative skewness in stock returns. European Journal of Finance, 11(6), 511-529. https://doi.org/10.1080/1351847042000286702

5. Harvey, C. R., & Siddique, A. (2000). Conditional skewness in asset pricing tests. Journal of Finance, 55(3), 1263-1295. https://doi.org/10.1111/0022-1082.00247

6. Jondeau, E., & Rockinger, M. (2003). Conditional volatility, skewness, and kurtosis: Existence, persistence, and comovements. Journal of Economic Dynamics and Control, 27(10), 1699-1737. https://doi.org/10.1016/S0165-1889(02)00079-9

7. Karoglou, M. (2010). Breaking down the non-normality of stock returns. European Journal of Finance, 16(1), 79-95. https://doi.org/10.1080/13518470902872343

8. Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263-291. https://doi.org/10.2307/1914185

9. Lim, A. E. B., Shanthikumar, J. G., & Vahn, G. Y. (2011). Conditional value-at-risk in portfolio optimization: Coherent but fragile. Operations Research Letters, 39(3), 163-171. https://doi.org/10.1016/j.orl.2011.03.004

10. Mandelbrot, B. (1963). The variation of certain speculative prices. Journal of Business, 36(4), 394-419. https://doi.org/10.1086/294632

11. Markowitz, H. (1952). Portfolio selection. The Journal of Finance, 7(1), 77-91. https://doi.org/10.1111/j.1540-6261.1952.tb01525.x

12. Takahashi, H., & Xu, P. (2016). Trading activities of short-sellers around index deletions: Evidence from the Nikkei 225. Journal of Financial Markets, 27, 132-146. https://doi.org/10.1016/j.finmar.2015.05.001

13. Peiro, A. (1999). Skewness in financial returns. Journal of Banking & Finance, 23(6), 847-862. https://doi.org/10.1016/S0378-4266(98)00119-8

14. Shah, S. A., Raza, H., & Hashmi, A. M. (2022). Downside risk-return volatilities during Covid 19 outbreak: A comparison across developed and emerging markets. Environmental Science and Pollution Research, 29(46), 70179-70191. https://doi.org/10.1007/s11356-022-20715-y

15. Rockafellar, R. T., & Uryasev, S. (2000). Optimization of conditional value-at-risk. Journal of Risk, 2(3), 21-42. https://doi.org/10.21314/JOR.2000.038

16. Rutkowska-Ziarko, A. (2023). Downside risk and profitability ratios: The case of the New York Stock Exchange. The North American Journal of Economics and Finance, 68, Article 101993. https://doi.org/10.1016/j.najef.2023.101993

17. Sortino, F. A., & van der Meer, R. (1991). Downside risk. The Journal of Portfolio Management, 17(4), 27-31. https://doi.org/10.3905/jpm.1991.409343

18. Thomas, N. M., Kashiramka, S., Yadav, S. S., & Paul, J. (2022). Role of emerging markets vis-à-vis frontier markets in improving portfolio diversification benefits. International Review of Economics & Finance, 78, 95-121. https://doi.org/10.1016/j.iref.2021.11.012

19. van Bilsen, S., Laeven, R., & Nijman, T. (2020). Consumption and portfolio choice under loss aversion and endogenous updating of the reference level. Management Science, 66(9), 3927-3955. https://doi.org/10.1287/mnsc.2019.3393

20. Yu, C., & Liu, Y. (2021). A personalized mean-CVaR portfolio optimization model for individual investment. Mathematical Problems in Engineering, 2021, Article 8863597. https://doi.org/10.1155/2021/8863597

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2026 Mohammed Faez Hasan

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

Authors retain the copyright of their papers without restrictions.