الفاعلية التكامليّة للمحاسبة الجنائية وأدوات الرقابة في تعزيز النزاهة المالية والإدارية

دراسة ميدانية

DOI:

https://doi.org/10.71207/ijas.v22i87.5612الكلمات المفتاحية:

المحاسبة الجنائية – الرقابة.الملخص

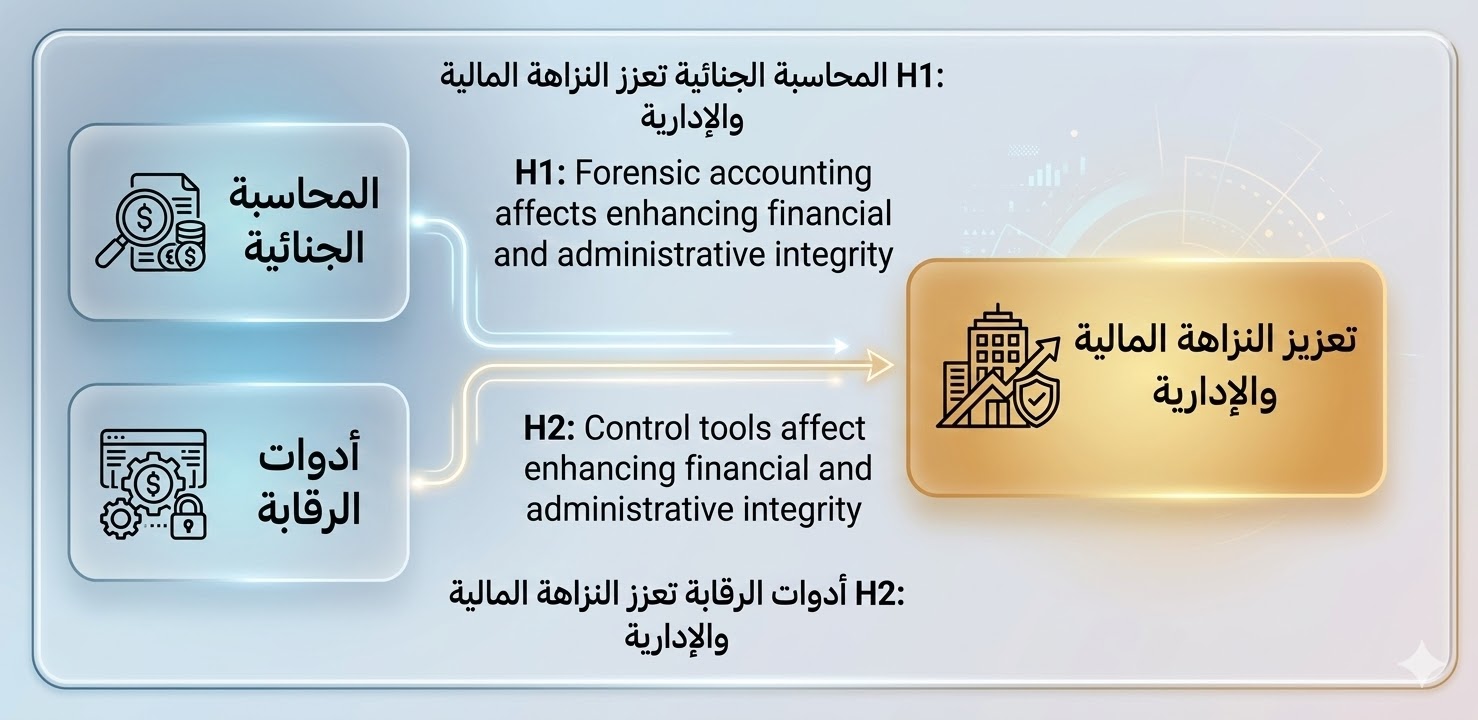

هدفت الدراسة إلى تحليل أثر تطبيق أدوات المحاسبة الجنائية على تعزيز النزاهة المالية والإدارية في المؤسسات الحكومية بمحافظة نينوى. تم اختيار عينة من موظفي المؤسسات الحكومية كممثل للمجتمع المستهدف، واعتمد البحث على المنهج التحليلي والإحصائي باستخدام برنامج SPSS، مع الاستناد إلى تحليل تقارير هيئة النزاهة لحالات الفساد الواقعية. أظهرت النتائج أن تطبيق أدوات المحاسبة الجنائية له تأثير إيجابي ومعنوي في تحسين الإجراءات الإدارية والمالية وتقليل التجاوزات، مع وجود عوامل أخرى تؤثر على النتائج. كما قدمت الدراسة توصيات لتعزيز تطبيق أدوات الرقابة وتدريب الكوادر وإنشاء آليات متابعة دورية لضمان الشفافية والكفاءة المؤسسية.

التنزيلات

المراجع

1. Alleyne, P., & Howard, M. (2005). An Exploratory Study of Auditors' Responsibility for Fraud Detection.

2. Ariffin, N., et al. (2021). Forensic Accounting and Risk Management: Exploring the Impact of Generalized Audit Software and Whistleblowing Systems on Fraud Detection in Indonesia.

3. Button, M., & Gee, J. (2013). Countering Fraud for Competitive Advantage: The Professional Approach to Reducing the Last Great Hidden Cost. Wiley.

4. Cochran, W. G. (1977). Sampling techniques (3rd ed.). New York: John Wiley & Sons.

5. COSO. (2013). Internal Control — Integrated Framework: Executive Summary. Committee of Sponsoring Organizations of the Treadway Commission.

6. DiGabriele, J. A. (2008). An Empirical Investigation of the Relevant Skills of Forensic Accountants. Journal of Education for Business, 83(6), 331–338.

7. DiGabriele, J. A. (2010). An Empirical Investigation of the Relevant Skills of Forensic Accountants. Journal of Education for Business, 85(6), 303–308.

8. FinanceStrategists.com. (2024). Skills and Qualifications of a Forensic Accountant. p. 1.

9. Gramling, A. A., Rittenberg, L. E., & Johnstone, K. M. (2012). Auditing: A Risk-Based Approach. Cengage Learning, 9th ed.

10. Hamawandy, N. M., Omer, A. J., & Salih, H. A. (2023). Role of internal audit in the public sector in Kurdistan Region of Iraq. Journal of Contemporary Issues in Business and Government

11. IARS International Research Journal. (2020). Forensic Accounting: A Way to Fight, Deter and Detect Fraud. p.

12. Integrity Forensic. (2023, June 27). Forensic Accounting vs Traditional Accounting: What’s the Difference? p. 1.

13. INTOSAI. (2020). Enhancing Government Accountability through Audit Reports. International Organization of Supreme Audit Institutions.

14. Investopedia (Dennis Madamba). (2003). Forensic Accounting: What It Is, How It's Used. p. 1–2. Available at https://www.investopedia.com/terms/f/forensicaccounting.asp Investopedia

15. Investopedia. (2008). Uncovering a Career in Forensic Accounting. p. 1–2. Available at

16. Investopedia. (2010). What Is a Forensic Audit, How Does It Work, and What Prompts It?

17. Jaeelo, K. A., & Ahmed, W. H. (2023). The role of accounting control in reducing financial and administrative corruption in cooperation between the external auditor and the internal auditor. Journal Port Science Research, 6(3), 273–285

18. Khan, S., & Ali, M. (2020). The Impact of Forensic Accounting Applications on Internal Control Effectiveness in Government Institutions.

19. Kranacher, M. J., Riley, R. A., & Wells, J. T. (2011). Forensic Accounting and Fraud Examination. Wiley.

20. Moeller, R. R. (2011). COSO Enterprise Risk Management: Establishing Effective Governance, Risk, and Compliance Processes. John Wiley & Sons.

21. OECD. (2019). Internal control and risk management for public integrity in the Middle East and North Africa. OECD Publishing

22. OECD. (2021). Government at a Glance 2021. Organisation for Economic Co-operation and Development.

23. Othman, R., Aris, N. A., Mardziyah, A., Zainan, N., & Amin, N. M. (2019). Fraud detection and prevention methods in the Malaysian public sector: Accountants’ and auditors’ perceptions. Journal of Financial Crime, 26(1), 72–88.

24. Power, M. (2019). Integrating Forensic Accounting with Big Data Technology in Internal Auditing. https://www.tandfonline.com/doi/full/10.1080/23311975.2022.2163560

25. Prasetiyo, R. et al. (2023). The Role of Forensic Accounting in Preventing Fraud and Corruption in the Public and Private Sectors. IARS International Research Journal, p. 16–17.

26. Prospects.uk. (2024). Forensic Accountant | Definition, Role, Education, Skills, Tools. p. 1. Available at https://www.prospects.ac.uk/job-profiles/forensic-accountant Prospects+1Finance Strategists+1

27. Raghavan, R., & Kumar, S. (2020). The Integration of Forensic Accounting and Big Data Technology Frameworks for Internal Fraud Mitigation in the Banking Industry.

28. Rezaee, Z. (2002). Financial Statement Fraud: Prevention and Detection. John Wiley & Sons.

29. Schouten, C. (2024). Unleashing the potential of public audits. INTOSAI Journal.

30. Transparency International. (2023). Global Corruption Barometer: Public Trust in Institutions.

31. TurningNumbers.com. (2024). Key Skills Every Forensic Accountant Should Have. p. 1. Available at https://www.turningnumbers.com/key-skills-every-forensic-accountant-should-have turningnumbers.com

32. UNDP، United Nations Development Programme. (2021). Corruption and integrity challenges in the public sector of Iraq. UNDP.

33. Vintti. (2025, January 8). Forensic Accounting vs Financial Accounting. p. 1.

34. Wells, J. T. (2011). Corporate Fraud Handbook: Prevention and Detection. 3rd ed., John Wiley & Sons.

35. World Bank. (2021). Supreme Audit Institutions Independence Index: 2021 Global Synthesis Report. World Bank.

36. تقارير مديرية تحقيق نينوى. (2020). منشورة على الموقع الرسمي لهيئة النزاهة.

37. الهيأة العامة للنزاهة (2023). ضبط موظفين في دائرة صحة نينوى لإحداثهم ضرراً بالمال العام عبر شراء أدوية دون عقود رسمية. هيئة النزاهة العراقية.

38. هيئة النزاهة (2021). تقرير الأداء السنوي لعام 2020، ص 41–45.

39. هيئة النزاهة الاتحادية. (2021, 20 حزيران). دائرة التحقيقات – مديرية تحقيق نينوى توقف بيع قطع أراضٍ حكومية (844 قطعة) وتضع إشارة عدم التصرف بقيمة 85 مليار دينار.

40. هيئة النزاهة الاتحادية. (2021, 3 تشرين الثاني). دائرة التحقيقات تكشف شبهات فساد إداري ومالي في مشروع إعادة تأهيل مستشفى السلام بمحافظة نينوى بقيمة تتجاوز 25 مليار دينار.

41. هيئة النزاهة الاتحادية. (2022، 28 آب). مديرية تحقيق نينوى تضبط مخالفات تنفيذية في عقود مشاريع حكومية تصل إلى أكثر من 44 مليار دينار.

42. هيئة النزاهة الاتحادية،(2023) ضبط 6 مسؤولين وموظفين في نينوى بتهمة الاحتيال عبر معاملات وهمية تجاوزت مليار دينار (9 شباط 2023)،

43. هيئة النزاهة العراقية. (2019). النزاهة تعلن ضبط اختلاس بأكثر من 11 مليار دينار من مخصصات نازحي نينوى. وكالة بغداد اليوم، وكالة الأنباء العراقية.

44. هيئة النزاهة العراقية. (2019). هيئة النزاهة تتهم محافظ نينوى السابق باختلاس 9.4 ملايين دولار.

45. هيئة النزاهة العراقية. (2020). السجن 15 عاماً لمختلس مليار ونصف دينار من أموال إعادة إعمار نينوى

46. هيئة النزاهة. (2023). اختلاس 64 مليون دولار قبل إقالة محافظ نينوى. موقع كردستان 24.

التنزيلات

منشور

كيفية الاقتباس

إصدار

القسم

الرخصة

الحقوق الفكرية (c) 2026 حسن صالح يوسف

هذا العمل مرخص بموجب Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

يحتفظ المؤلفون بحقوق الطبع والنشر لأوراقهم دون قيود.