Events subsequent to the date of the balance sheet and their impact on the veracity of the financial statements - a field study in the General Company for Industries

Keywords:

Balance sheet, the truth about financial statementsAbstract

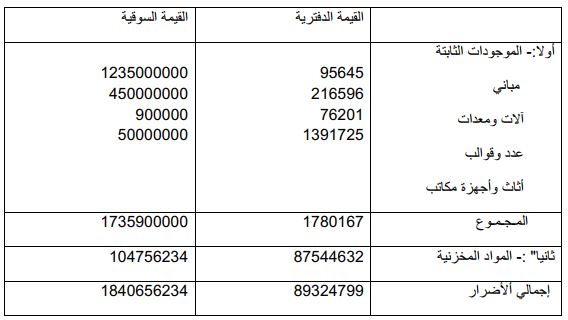

Accounting plays an important role in economic and social life through the production of accounting information and its presentation in financial statements. The research problem stems from the existence of a cut-off period between the date of the balance sheet and the date of approval of the issuance of the financial statements. During that period, important events may occur that have a fundamental impact on assets or liabilities. related to the company or events occur that affect the company’s ability to continue its activity, and these events are called subsequent events. Failure to consider these events when publishing the financial statements leads to the financial statements being misleading and not expressing the true financial position of the company and those affecting the decisions of the users of those financial statements. The research focuses On the events that accompanied the war on Iraq in 2003 and the resulting damage to the General Company for Textile Industries / Babylon (research sample) and how to address them accountingally in harmony with local and international accounting standards. These events are classified into two types: -

1- Events that provide additional evidence about conditions that existed at the date of the balance sheet and are described as events that require modification, meaning that assets and liabilities must be modified and disclosed in the financial statements.

2- Events that arose after the balance sheet date and provide evidence of cases that did not exist when preparing the balance sheet. They are described as events that do not require amendment, and we limit ourselves to disclosure in the financial statements. Among the means used to disclose events after the balance sheet date of the basic financial statements are explanatory notes, the auditor’s report, and the management report.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2010 College of Administration and Economics - University of Kerbala

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

Authors retain the copyright of their papers without restrictions.