Conditioning of accounting disclosure of commercial banks according to the requirements of the relevant international standards to financial instruments and display - An Empirical Study

Keywords:

Conditioning Accounting disclosure Of commercial banks The requirements of international standards Financial instruments and displayAbstract

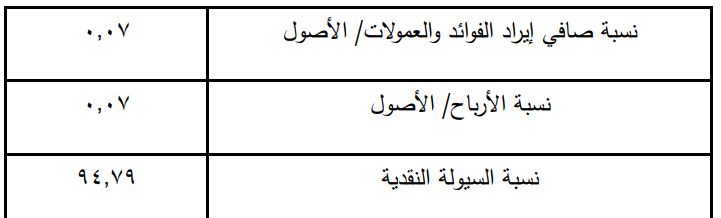

Contributes to the application of international standards to improve the quality of accounting information provided to the parties to the recipient through the provision of appropriate information and are subject to the understanding and comparison and with high reliability. As for the banks a special nature in terms of the activities of, and risks to that which prompted the international committees to develop independent criteria for the disclosure of accounting in financial reports and statements of their own and which will prepare the input necessary to gain access to information that helps decision makers to assess the financial position and results of business for banks business. And helps the application of international standards for the preparation of financial reports by the commercial banks to consolidate the basis for preparing financial statements and disclosures in accordance with the methods of preparation and disclosure of the global banks. And research deals with the current examination of reports and financial statements of Commercial Bank in the province of Sulaymaniyah, Kurdistan Region of Iraq for the financial year (2006) and prepared in accordance with the accounting system common for banks and insurance companies on the identification of shortcomings, and then work to adapt them in line with both the international number (1) Presentation of financial statements and the international standard for financial reporting number (7) (Financial Instruments: Disclosures). By identifying the aspects that belong to the accounting disclosure under the criteria, which has never suffered the financial statements of the Bank under discussion, analysis, and of the necessity of organizing the cash flow statement and record financial instruments at fair value and indicate the amount of change where and to whom is attributed to changes in credit risk.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2010 College of Administration and Economics - University of Kerbala

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

Authors retain the copyright of their papers without restrictions.