The quality of the auditor’s report in light of international and local auditing standards - a comparative study with the development of a proposed model for amending the Iraqi Auditing Manual No. (2)

Keywords:

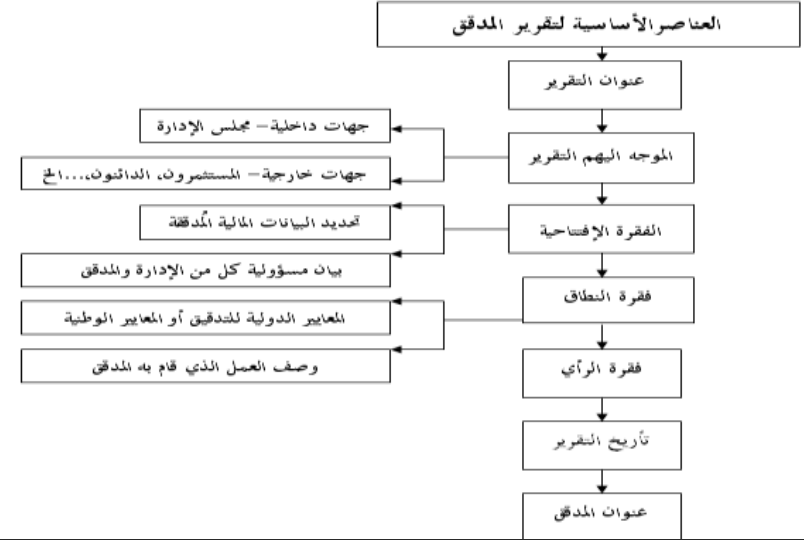

Quality of the auditor’s report, ,International auditing standardsAbstract

The research aims to find a comparative analysis for the International Auditing Standards \"Modified\" No. (700,705,706) related to the Auditor\'s report about the financial data which issued by the International federation of Accountants 2010 with the Iraqi Audit Guide No. (2) Which issued by the Council of Auditing & Accounting Standards in Iraq 1999 to find out the extent of its compatibility or differences in addition to measure the range of points of views of their prepared persons and suggest a \"modified\" Iraqi Auditing Guide according to the comparative results.

The research found several conclusions mainly is that the auditor should take into consideration the International & Iraqi Audit Standards when preparing his report in order to insure quality in that report.

One of the most prominent of research\'s recommendations represent that it is necessary for institutions which are responsible for professional work in Iraq should exert more effort to renew the Iraqi Audit Standards mainly Audit Guide No.2 of auditor\'s report and developed them in order to be compatible with the new requirements of auditing career.

References

- Bank for International Settlements(BISs), "External audit guality and

banking supervision", Press & Communications CH- 4002 Basel, Swizerland,

Available at: htt://www.bis.org/publ/bcbs146.pdf.

- De Angelo, L.E.," Auditor size and audit. Guality", Journal of Accounting

and Economics, 3(December), 1981.

- Solomon, D., "An Information Economics analysis of Financial Reporting

and External Auditing", The Accounting, 1978.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2013 Economics and Administration College - Karbala University

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

Authors retain the copyright of their papers without restrictions.